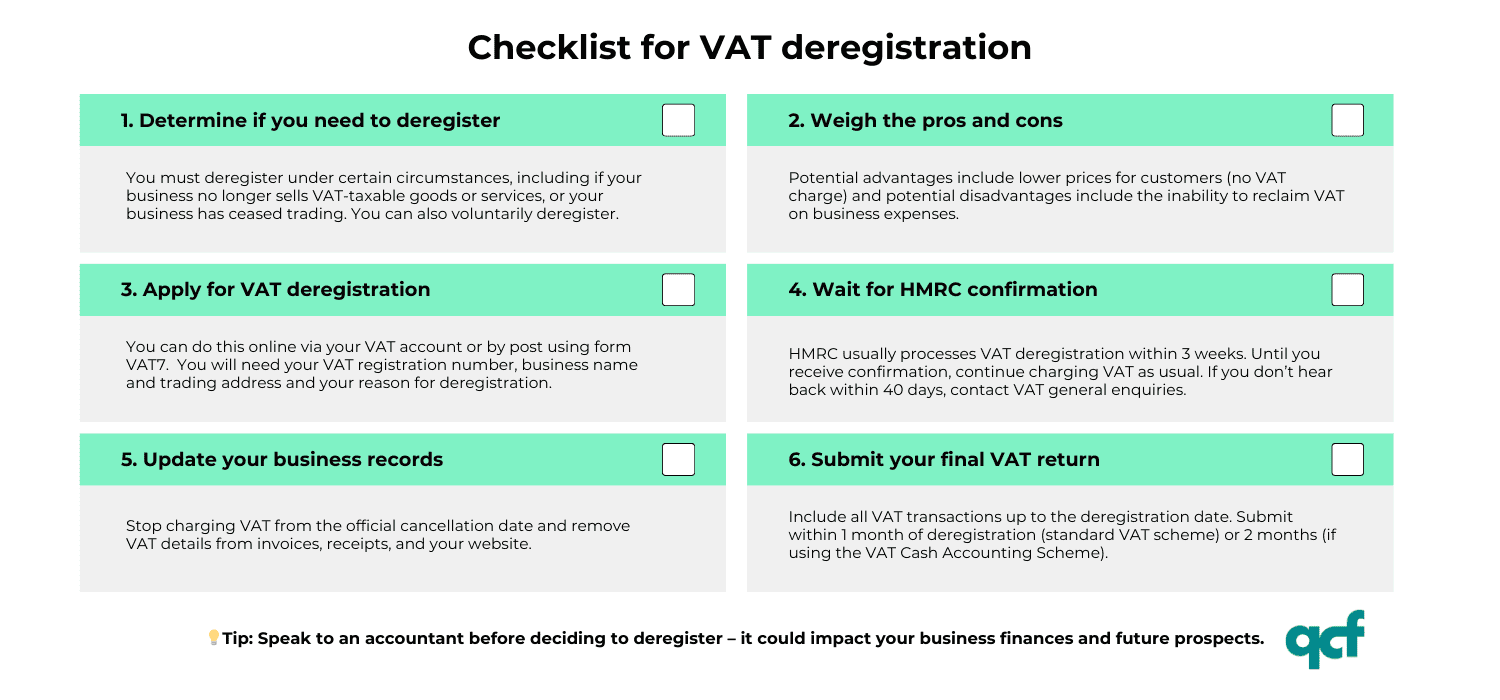

If your business is no longer eligible for VAT registration, you must apply to HMRC to deregister for VAT – i.e. cancel your registration. You can also choose to deregister voluntarily at any time if your VAT-taxable turnover is below £88,000.

In this guide, we explain what VAT deregistration means, the common reasons why a business may need or want to deregister, and the steps you need to take to successfully cancel your VAT registration with HMRC.

Key takeaways

- Businesses must deregister for VAT if they stop selling VAT-taxable goods, cease trading, or join a VAT group. Voluntary deregistration is also possible if turnover falls below £88,000.

- Deregistering removes the need to submit VAT returns and can lower the prices you charge, but you also lose the ability to reclaim VAT on purchases.

- The VAT deregistration process takes around three weeks. Your business must continue charging VAT until HMRC confirms deregistration.

What does it mean to deregister for VAT?

From 1 April 2024, businesses must register for VAT with HMRC when their annual VAT-taxable turnover exceeds £90,000, or they expect to exceed this threshold in the next 30 days.

This rule applies to all types of legal structures, including limited companies, limited liability partnerships (LLPs), general partnerships, and sole traders.

Voluntary VAT registration is also possible for businesses with an annual turnover below the VAT registration threshold.

- When should I register for VAT?

- How do I get a company VAT number?

- A guide to using HMRC’s new VAT Registration Estimator tool

However, there are a number of situations where a business may want to cancel its VAT registration, or be legally required to do so. This process of cancelling VAT registration is often referred to as deregistering for VAT.

If you need or want to deregister for VAT for any reason, you must apply to HMRC online or by post. You will also need to make a number of changes to your business, including no longer charging VAT on the goods or services you provide.

Why would a business deregister for VAT?

There are several reasons why a business would apply to deregister for VAT. Some of these are compulsory, whilst others are voluntary.

Compulsory VAT deregistration

By law, you must cancel your VAT registration within 30 days if your business meets at least one of the following conditions:

1. No longer offers VAT-taxable goods or services

You can only charge VAT if your business trades or makes taxable supplies, i.e. if you sell VAT-taxable goods or services to customers.

If you stop selling supplies that attract VAT and you have no intention of doing so in the future, you are no longer eligible for VAT registration and cannot charge your customers VAT.

It may also be the case that you registered for VAT with the intention of selling taxable goods, but the plan never came to fruition. This often happens with startups.

2. Your business ceases trading

If you stop trading through your business, you are legally required to notify HMRC and cancel your VAT registration.

This could be as a result of you looking to permanently close your business or if you make your company dormant and don’t intend to trade again.

3. You sell your business

If you decide to sell your business, you may need to cancel your VAT registration. However, if the new owner wishes to continue using the same VAT number, you can transfer your VAT registration instead.

4. Change of legal structure

Some existing businesses change their legal structure – for example, from sole trader to limited company and vice versa. In this situation, you must cancel the VAT registration for your original business structure if you want a new VAT number for your new structure.

However, during the deregistration process, you have the option of transferring your VAT registration to your new business structure. This will allow you to keep your existing VAT number.

5. Your business joins a VAT group registration

Your business cannot have more than one active VAT registration. Therefore, if you create or join a VAT group, you will need to cancel your individual VAT registration.

The group will have its own VAT number, under which one member company will collect, report, and pay all future VAT for all members of the group.

6. You intend to join the Agricultural Flat Rate Scheme

The Agricultural Flat Rate Scheme is an optional alternative to VAT registration for farmers.

If you want to join the scheme and your business is registered for VAT, you must cancel your VAT registration if your turnover for non-farming goods and services is below £90,000.

Voluntary VAT deregistration

If your VAT-taxable turnover falls below £88,000 (the VAT deregistration threshold), you can apply to HMRC to cancel your registration unless:

- You and your business are based outside the UK, and

- You supply any goods or services to the UK (or expect to do so the next 30 days)

It is set at £2,000 below the VAT registration threshold to prevent businesses from opting in and out of registration when their taxable turnover fluctuates by only minimal amounts.

The most common reason why a business may choose to cancel its VAT registration is that its taxable turnover has fallen below the threshold and VAT registration is no longer beneficial. This could be as a result of:

- reducing your opening hours

- losing a major client

- lowering your prices

- expiry of valuable contracts

- ceasing production of a particular product

- changing the types of products or services you sell

- drop in demand within your particular industry

- prolonged recovery after the loss of business during Covid lockdowns

You can also cancel if you’re applying for an exemption because your taxable supplies are solely or mainly zero-rated for VAT.

You must provide a specific reason and be able to satisfy HMRC that your VAT-taxable turnover in the following 12 months will remain below the cancellation threshold of £88,000.

To do so, you will need to analyse your turnover forecasts for that time period, considering any eventualities that could generate additional income and push your taxable turnover over the threshold.

If you are a retail business, you must also confirm to HMRC that you will reduce the prices you charge by the VAT element.

If you opted for voluntary VAT registration, there may simply come a time when it is no longer beneficial to your business. For example:

- The administrative burden outweighs the advantages of being able to charge VAT

- Your business incurs very little input VAT (the VAT you charge on the goods or services you sell)

- Some or all of your customers are not VAT-registered (e.g. retail customers), so they cannot recover the VAT you charge

- Charging VAT makes your products or services appear too expensive and the business cannot afford to absorb the cost

VAT is a complex area, so you should carefully weigh up the pros and cons of cancelling your VAT registration before making a decision.

Advantages and disadvantages of VAT deregistration

Depending on your situation, there are several possible advantages to deregistering for VAT:

- You can lower your prices and gain a competitive advantage

- Attract more non-VAT registered customers

- You don’t have to obtain and keep VAT receipts for purchases you make through the business

- No requirement to prepare and submit quarterly VAT Returns to HMRC

- Simpler accounting and record-keeping requirements

On the flip side, there are a number of disadvantages associated with VAT deregistration:

- You will not be able to reclaim the VAT you pay on any products or services you buy for the business

- Some companies only work with other VAT-registered businesses. Deregistering could reduce the pool of clients and suppliers who are prepared to work with you

- Existing clients may perceive deregistration as a sign that your business is in trouble or not performing as well as it did in the past

- Not being VAT-registered can make your business appear too small or less credible to prospective clients

- You will have to closely monitor turnover on a monthly basis to avoid going over the VAT registration threshold

- It may limit the growth of your business

If you are considering voluntary VAT deregistration, we would advise speaking to your accountant in the first instance. They will be able to provide expert help and guidance specific to the needs of your business.

How to cancel your VAT registration

If your business meets the criteria for VAT deregistration, you can apply to HMRC in one of two ways:

- through your VAT online account

- by completing form VAT7 and submitting it by post

1. Deregister online

To deregister for VAT online, you will need your Government Gateway user ID and password. Upon signing in, select ‘deregister for VAT’ and follow the prompts.

During the process, you will be asked to provide the following details:

- VAT registration number

- The full, official name of the business (i.e. company name or trading name)

- Principal place of business (i.e. your company’s main trading address)

- Contact telephone number

- Reason for deregistration – additional information may be required, depending on the reason

- The date on which you will cease to trade, stop making taxable supplies, or want to deregister (whichever applies)

The form must be completed by one of the following individuals:

- The sole owner of the business

- One of the partners, if there is more than one owner

- Director or company secretary

- An officer or official applying on behalf of an unincorporated body, e.g. a secretary or trustee

- An authorised agent – HMRC must be aware that the agent has been authorised to act on behalf of the business

How long does the VAT deregistration process take?

After applying to cancel your VAT registration, you should receive a reply from HMRC within three weeks. However, it can sometimes take longer, especially during busy periods or if HMRC requires further information.

During this time, you must continue to charge VAT as usual. If you do not hear back from HMRC within 40 days of sending your application, you should contact VAT general enquiries on 0300 200 3700.

If HMRC approves your application, you will receive a formal notice in your VAT online account to confirm the official date of your VAT deregistration.

This will be the date on which the reason for deregistration took effect (e.g. when you ceased trading), or the date you asked to cancel.

2. Deregister by post

To deregister for VAT by post, you must complete form VAT7. You will need to fill in this form online, print it, and send it to HMRC at the address shown at the end of the form.

If HMRC approves your application, you will receive a formal confirmation notice through the post.

You cannot use this form if you are selling your business or changing its legal structure and want to transfer the existing VAT registration number.

Please refer to HMRC’s VAT Notice 700/11: Cancelling your registration for detailed guidance on deregistration in these situations.

Your responsibilities after VAT deregistration

You must stop charging VAT on your products and services from the cancellation date stated on the notice you receive from HMRC.

Consequently, you will have to change your invoices and any other documentation that contain your VAT registration number. Where applicable, this may include websites, emails, and till receipts.

The confirmation notice will become part of your VAT records. You must retain it, along with all other VAT records, for a period of 6 years.

You will have to submit a final VAT Return to HMRC for the period of time up to and including the date of deregistration.

Also account for any stock and other business assets that you own on this date if:

- you reclaimed, or could have reclaimed VAT when you purchased the assets, and

- the total VAT due on these assets is greater than £1,000

The deadline for filing your final VAT Return is one month after the cancellation date, unless you are using the VAT Cash Accounting Scheme.

If you use this scheme, you must submit your final return within two months of the cancellation date.

There is no need to wait until you receive all of your invoices before filing your final VAT Return. You will still be able to reclaim VAT when you receive them, provided the VAT charges occurred within the past four years.

Re-registering for VAT

HMRC will automatically re-register your business for VAT if they discover that cancellation should not have taken place. If this happens, you will need to account for any VAT payments that you should have been making during the period of deregistration.

If your business becomes liable for VAT registration at some point in the future, or you decide that you want to re-register voluntarily after cancellation, you can simply complete a new VAT registration online. However, you won’t receive the same registration number.

Can I transfer my VAT registration?

In certain circumstances, you can transfer your VAT registration number if there is a change of business structure or ownership. For example:

- you change the legal status (structure) of your business, e.g. convert from sole trader to limited company

- you buy/sell an existing business as a going concern and the new owner wants to retain the VAT registration number

You can apply to HMRC for a VAT registration number transfer by post. It usually takes HMRC around three weeks to confirm a transfer.

When changing the legal status of your business

If you want to transfer your VAT registration number upon changing the legal status of your business (also known as a ‘change of legal entity’), you must:

- Print, complete, and post form VAT68 to HMRC, then

- Register for VAT

When selling or buying an existing business

To transfer a VAT registration number upon selling or buying a business as a going concern, the following steps are required:

- The seller and purchaser must complete form VAT68 – print, complete, and post the form to HMRC

- The buyer must register for VAT

HMRC will treat form VAT68 as the seller’s cancellation and then transfer the VAT registration to the buyer. The seller does not need to complete form VAT7.

Seek professional tax advice

Whilst the process of cancelling VAT registration is relatively straightforward, the decision and accompanying steps may be less so in certain situations. This is especially true for businesses that choose to cancel voluntarily.

When you deregister for VAT, your accounting and record-keeping duties will certainly reduce, but it could have a damaging effect on your business finances, commercial appeal, and future prospects.

Determining the potential implications can be tricky for many people. Therefore, we would urge you to seek professional advice from an accountant before making a decision on whether or not to deregister for VAT.

Go to Quality Company Formations for support registering for VAT

If you would like support registering for VAT, or if you need help forming a company, please leave a comment below or get in touch with our company formation team.

Check out our other Quality Company Formations blogs for more information on the tax and accounting aspects of running a business.

Join The Discussion

Comments (4)

Hi VAT team,

I completed the online VAT de-registration form prematurely as the sale of the asset, which would have reduced turnover, has now fallen through.

The form (via the Gateway) was completed on the 1st August to be effective 1st August 2023. Company – Strathardle lodge Ltd SC711685.

I would be grateful for your guidance as to how to cancel the de-registration request?

Kind regards,

David Brice (Director)

Thank you for your kind enquiry, David.

We would recommend you urgently contact HMRC’s VAT General Enquiries phone line on: 0300 200 3700.

Sorry we cannot be of more assistance.

Kind regards,

The QCF Team

Hi,

I am writing to seek your professional advice regarding the VAT status of our company. Our business was initially started as a sole trader, and after a few months of operation, it was shifted to a Limited Company (LTD)”TRENDY GIFT SHOP LTD”.

As a sole trader, This business was VAT registered, and after the transition to an LTD, Previous beneficary owner/director/ failed to obtain a VAT deregistration from the sole trader. Later on, the beneficiary owner of the company was changed, and the business is still being charged VAT, even though the company is not VAT registered.

We have recently discovered this issue and would like to rectify it as soon as possible. We want to apply for VAT exemption for our Ltd since it was never registered for VAT, and the previous director/beneficiary owner was only VAT registered in his sole trader capacity.

We would appreciate it if you could guide us through the process of obtaining VAT exemption for our company and assist us in ensuring that we comply with all the necessary legal requirements. We would also be grateful if you could advise us on any possible penalties that we may face for this oversight.

Thank you for your time and attention to this matter. We look forward to hearing from you soon.

Sincerely,

Trendy Gift Shop ltd.

Thank you for your kind enquiry, Muhammad.

Unfortunately we are unable to advise on this, given the complexity of the situation. We would recommend you seek the advice of an appropriate accountant.

We are sorry we could not be of more assistance on this occasion.

Kind regards,

The QCF Team