The ownership of limited companies can change at any time. It happens whenever new members (shareholders or guarantors) join a company or when existing members leave. Below, we explain how to add company shareholders after incorporation and how to record and report such changes.

Whenever there is a change in ownership, the directors should ensure that the appropriate statutory registers are updated and that Companies House is informed of the change when the next confirmation statement is filed.

Key takeaways

- Update statutory registers promptly to reflect changes in shareholders and ensure compliance with Companies House regulations.

- Understand pre-emption rights to maintain control over share ownership and prevent unwanted transfers to outsiders.

- Directors may require shareholder approval for share transfers if they lack the authority to authorize changes independently.

How to add company shareholders after incorporation

You can add new shareholders after company formation by issuing (allotting) more shares as well as by transferring existing ones. There are many reasons why a company may choose or need to do this, such as:

- A shareholder dies

- A shareholder wishes to retire or redeem his or her investment

- The company needs to raise capital to further its aims

- To bring in business partners and grow the company

- To introduce an employee share scheme

- An existing shareholder wants to transfer shares to a family member as a gift or tax-planning strategy

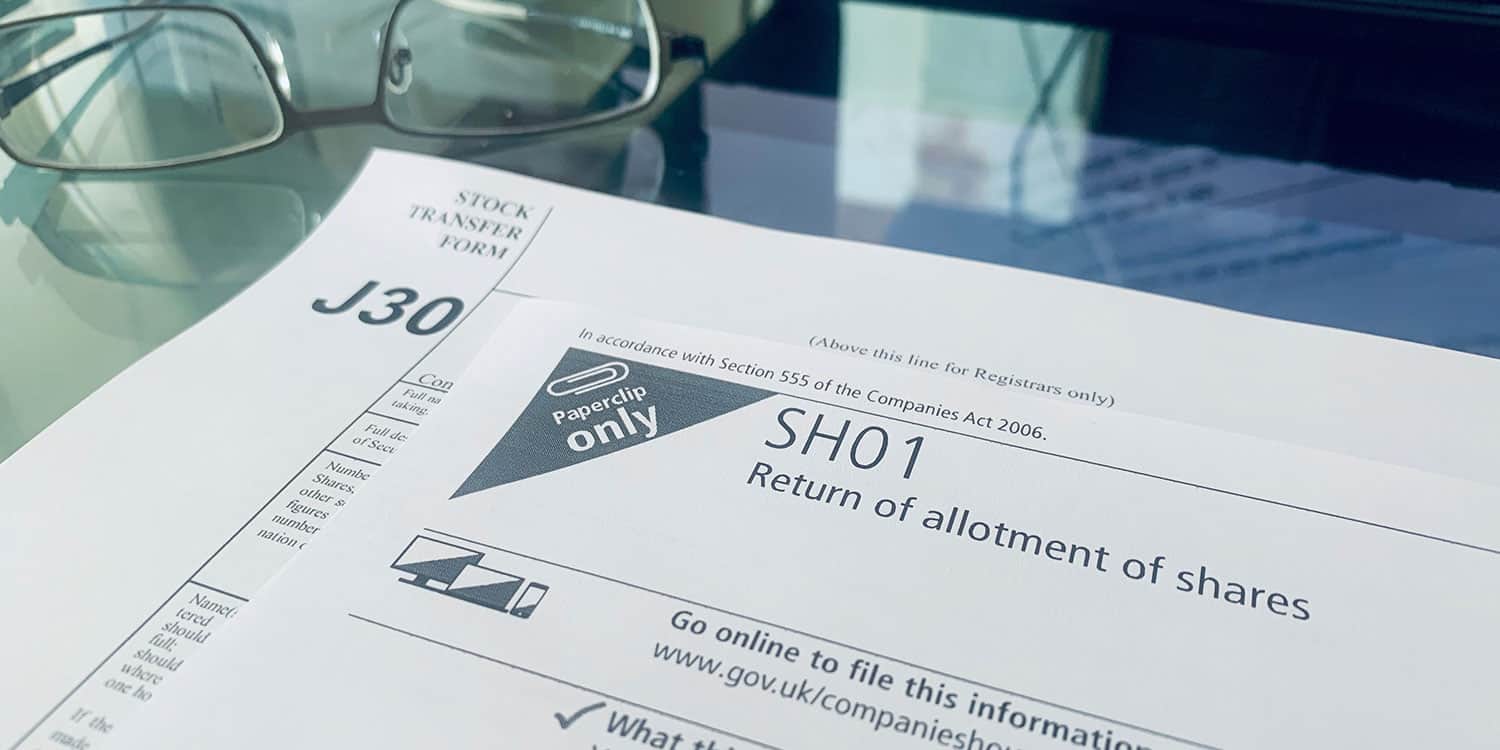

Transferring shares

Existing company shares can be sold or gifted from current members to new shareholders at any time. To do so, you must complete a Stock Transfer Form for acceptance by the board. This is a relatively straightforward procedure in most cases.

When the transfer is complete, the director should issue a share certificate to the new member and update the statutory register of members. You may also have to update the register of People with Significant Control (PSC).

Companies House must then be notified about the change in share ownership and PSC information on the next confirmation statement.

Allotting new shares

If you wish to sell or gift shares and you do not want to transfer any existing shares, the company will have to allot more shares. This will increase the total share capital of the company, but it will dilute the proportional value of the existing shares.

To issue new shares, an application should be made to the Company, the board must accept the allotment, and a Return of Allotment (Companies House form SH01) should be completed with the following details:

- Company registration number

- Company name in full

- Allotment date

- Shares allotted (currency, class, quantity, nominal value, amount paid or unpaid on shares)

- Details of non-cash consideration (if applicable)

- Statement of capital (updated table showing all issued shares in the company)

- Rights attached to shares

Form SH01 must be sent to Companies House no later than one month after the allotment date. The director is then responsible for issuing a share certificate to the new member, updating the company’s register or members and PSC register (if applicable), and notifying Companies House of the new shareholder (and PSC, if applicable) on the next Confirmation Statement.

Restrictions on the transfer or allotment of shares

The articles of association and shareholders’ agreement often contain clauses that restrict the transfer or allotment of shares in certain circumstances. This is why it is important to refer to these documents before any transfer or allotment is authorised.

The most common restrictions include

- pre-emption rights of existing members

- authorised share capital

- director’s power to authorise transfers and allotments

- buy-back options of the company

Members have the right to include and amend any such restrictions at any time by passing a special resolution at a general meeting.

Pre-emption rights

Many companies stipulate pre-emption rights on the transfer or allotment of shares, which means that any shares that become available must then be offered to existing members for first refusal. Shares can only be transferred to other people if members waive their pre-emption rights.

The purpose of pre-emption rights is to ensure that shareholders are able to maintain their current percentage of ownership and control. These rights also help to prevent unsuitable persons acquiring a controlling interest in the business.

Authorised share capital

This is a clause that sets a limit to a company’s total share capital by restricting the number and value of issued shares to a fixed sum.

Prior to the introduction of the Companies Act 2006, this restriction was compulsory, and new companies had to pay Stamp Duty in relation to their issued share capital. This is no longer the case, so very few companies choose to restrict their share capital now.

Director’s power to authorise share transfers and allotments

Members choose which powers to grant to directors. Sometimes this includes the power to authorise share transfers and allotments, especially when shareholders and directors are the same people. However, many shareholders prefer to retain this power because it directly impacts their level of control and profit entitlement.

If a director does not have the power to authorise share transfers and allotments, existing members must approve the transfer or allotment themselves by passing a resolution at a general meeting or in writing.

Buy-back options of the company

Buy-back options are often included in the articles or shareholders’ agreement allowing for the shares to be purchased (and cancelled) by the company.

This means that the company has the right to buy back shares when a director or employee leaves a company, thus ensuring that any beneficial ownership cannot be retained by someone who is no longer working for the business.

Updating statutory company registers

When a shareholder joins a company, it is very important to update the required statutory registers. These are usually kept at the registered office address.

The register of members must be updated to reflect, where applicable:

- name & address of new shareholder

- date on which they joined or left the company (this will be the date on which new shares are taken or existing shares are transferred to someone else)

- details of share(s) taken or transferred (currency, class, quantity, nominal value, amount paid or unpaid on shares)

If the new or existing shareholder is also a person with significant control, the PSC register must be updated to reflect the new PSC or the date on which the existing member ceased being a PSC of the company.

Reporting shareholder changes to Companies House

Companies House must be informed when there is any change to shareholder or share details. This information is then reported on the confirmation statement and published on public record.

You can wait to submit this information until it’s time to file your next confirmation statement, or you can report these changes sooner by updating the statement immediately.

It’s usually recommended to send in the confirmation statement as quickly as possible following the change, particularly if the company is applying to set up a bank account.

To report a new shareholder, you must also provide their name and details of the shares they hold (class and quantity). There is no need to provide an address. To report a share transfer, you must also note the number of shares transferred and the transfer date.

To report a new PSC, you must also provide their name, country/state of residence, nationality, month and year of birth, service address, and the date on which they became a PSC.

If someone ceases to be a PSC, you must also provide the aforementioned information and the date on which they stopped being a PSC. The PSC information is updated on Companies House using the PSC01-09 forms.

Join The Discussion